Brand new get back away from 100% mortgage loans has been promoted as a way to assist beleaguered first-day consumers get onto the possessions steps, and one of the very most visible profit recently got smaller since the Barclays keeps cut costs for the the 100% guarantor financial.

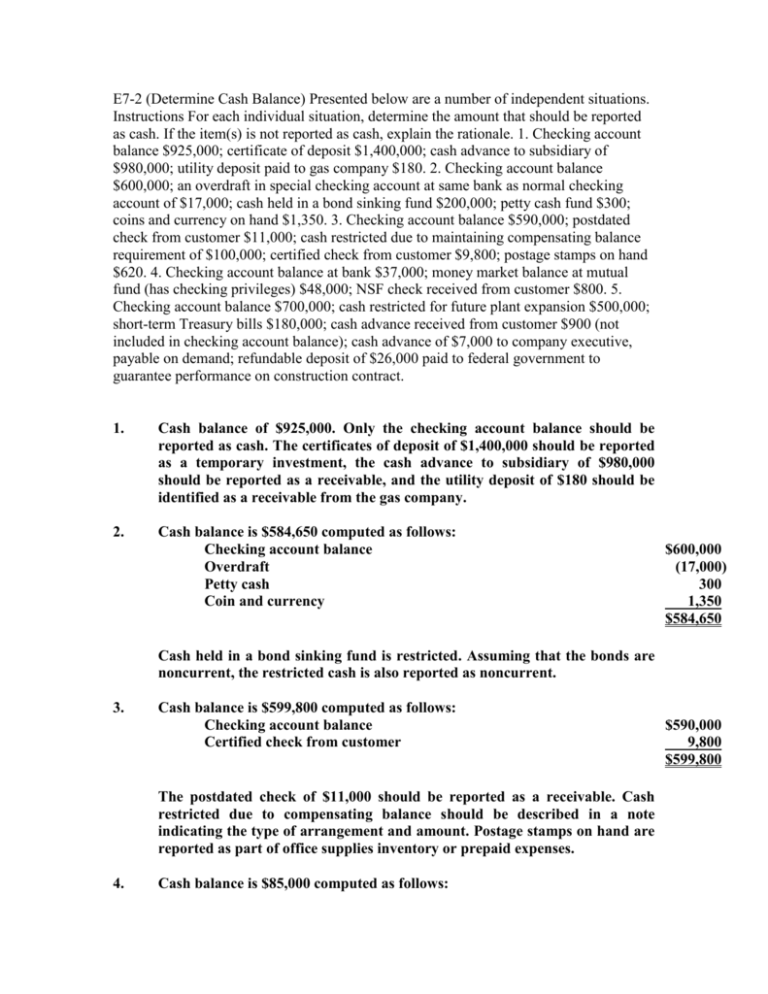

Brand new bank’s 100% Family relations Springboard financial, and that doesn’t need new borrower to place down a deposit, is now offering a lower speed of 2.95% away from 3% prior to now. This will make it less expensive than large-road rival Lloyds Bank, and therefore released the same offer earlier this season .

In addition helps to make the bargain less expensive than of many 95% loan-to-value (LTV) mortgages, hence wanted consumers to place down in initial deposit with a minimum of 5%.

Mortgages enabling you to obtain 100% out-of a property’s really worth was considered becoming a major contributor toward property crisis away from 2008, however, over a decade after, are they worth taking into consideration?

Hence? examines the brand new 100% home loan field, and you can explains advantages and you may dangers of the new questionable money, how many payday loans can you have out in Michigan that have viewed a resurgence in 2010.

Be much more currency experienced

That it newsletter delivers free currency-relevant blogs, along with other information about Hence? Group products. Unsubscribe anytime. Your computer data will be processed according to all of our Privacy policy

What is an excellent 100% home loan?

Good 100% home loan is actually a loan for the entire price away from a great possessions, and therefore doesn’t need new borrower to pay a deposit.

not, they would nevertheless possibly have to pay to own stamp obligation (regardless if you will find none charged so you’re able to first-time buyers buying qualities worthy of around ?3 hundred,000), plus financial and you can judge costs, as well as the cost of a home questionnaire .

While they’re named ‘ 100% mortgages ‘, this new revenue constantly require a dad otherwise loved one to act as the a good guarantor and are usually commonly known as guarantor mortgage loans.

The structure Societies Connection (BSA) recently mentioned that lenders must look into taking back the high-risk loans, and that played a member regarding the 2008 economic crash, to eliminate customers relying on its moms and dads.

How does Barclay’s 100% mortgage performs?

It need a 10% put on the borrower’s mothers, and that’s came back after three years, provided all of the mortgage repayments are available promptly.

Barclays will pay 2.27% AER yearly of your own three-seasons period. In comparison, Lloyds Lender will pay dos.5% AER towards the the comparable package.

What kinds of 100% mortgage loans come?

Usually, 100% mortgage loans are only readily available for those who have a good guarantor, always a pops who will protection the mortgage if you skip a cost.

- Find out more:100% mortgage loans

100% mortgages: positives and negatives

The main advantage of a great 100% home loan is you won’t need to glance at the strive from extract together in initial deposit having home financing.

So that as much time since you meet all of your mortgage payments, there is no pricing to your guarantor. They may even be advisable for those having reasonable profits, otherwise with a less than perfect credit history.

But many therisk consist for the guarantor, just who sometimes need create her home because the security in order to straight back the individual taking out fully the fresh new 100% mortgage. As a result the brand new guarantor’s house was at risk if brand new borrower doesn’t create costs.

Another significant disadvantage is actually bad guarantee , where you are obligated to pay much more about the home loan versus home is well worth. Which have an effective 100% home loan, a dip on possessions rate often quickly suggest the home loan is higher than the value of your residence. Thanks to this of many lenders are also unwilling to offer 100% deals.

From the nearest and dearest offset mortgage, the family user wouldn’t secure any desire to their deals, while on a mutual mortgage the household representative will need to shell out stamp obligations at the most price and you may face capital increases income tax expenses.